Plan Sponsor Resources

Retirement Plan Administration

.png)

.png)

Categories:

Congratulations on your decision to sponsor a retirement plan - one of the most valuable benefits you can deliver to your employees! While you can expect a number of significant rewards from your efforts, your plan’s fiduciaries must be careful to comply with some of the most technical and consequential rules and regulations under the law.

In order to protect employees’ savings, the Employee Retirement Income Security Act of 1974, as amended (ERISA) mandates that any person(s) responsible for managing or administering a retirement plan (the plan’s “fiduciaries” or “you”) act prudently. The Department of Labor (DOL) is tasked with periodically investigating ERISA-covered plans to ensure the fiduciaries are complying with applicable laws and regulations.

When it comes to selecting investments for the plan, ERISA requires fiduciaries to follow an objective process, which takes into account the needs of the plan’s participants, in order to make well-informed decisions. Fiduciaries are required to consider relevant information (or that which they should know to be relevant) about the investment options available to the plan and to designate an appropriate number of different types of investments such that participants can create well-diversified portfolios to minimize the risk of large losses.

Where the plan’s fiduciaries lack the necessary investment-related expertise to make informed decisions, ERISA requires them to hire professional assistance. Hiring an experienced plan consultant will help ensure you meet your fiduciary duties, and he/she will often have specialized knowledge and tools to streamline the investment selection and review process

OVERVIEW OF FIDUCIARY RESPONSIBILITIES

ERISA requires plan sponsors to act prudently when making decisions relating to the management or administration of the plan. These “fiduciary functions” must be performed solely in the interests of plan participants and beneficiaries, with the exclusive purpose of providing benefits, while defraying reasonable expenses. In addition, when it comes to selecting investment options, plan fiduciaries have a duty to diversify investments and defray reasonable expenses.

Some plans, such as most 401(k) and profit sharing plans, can be set up to give participants control over the investments in their accounts and limit a fiduciary’s liability for the participants’ investment decisions. For participants to have control, they must be given the opportunity to choose from a broad range of investment alternatives.

According to the DOL, the plan fiduciaries must designate at least three different investment options so that employees can diversify investments within an investment category, such as through a mutual fund, and diversify among the investment alternatives offered. Participants must also be given sufficient information to make informed decisions about the options offered under the plan.

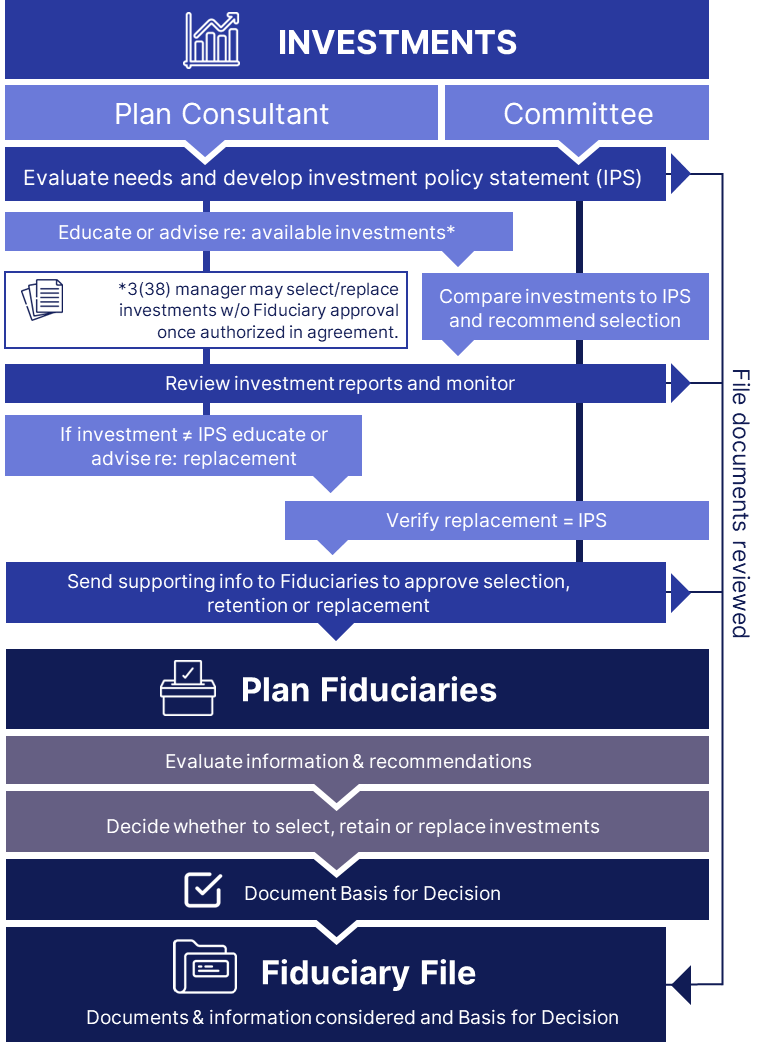

Given that most plan sponsors lack the requisite investment-related experience, it is quite common for the fiduciaries to engage outside assistance. If you don’t have the internal resources to properly evaluate the number and types of asset classes that are appropriate for your participants and/or to track then performance and costs associated with each designated investment alternative (DIA), then you should consider engaging third-party assistance. Unless you have properly delegated your investment-related duties to an “investment manager,” then you should designate at least one person on the plan committee to work with an investment professional to ensure the DIAs are prudently selected and monitored, and if necessary, replaced.

A prudent investment selection process begins with an objective approach to reviewing each investment option that is being considered for the investment line-up, taking into consideration the performance of a fund relative to its peers, market benchmarks and expenses. Most plans elect to adopt an investment policy statement (IPS) to provide a consistent and repeatable process for selecting, monitoring and replacing the plan’s DIAs.

ADOPTING ADOPTING AN INVESTMENT POLICY STATEMENT

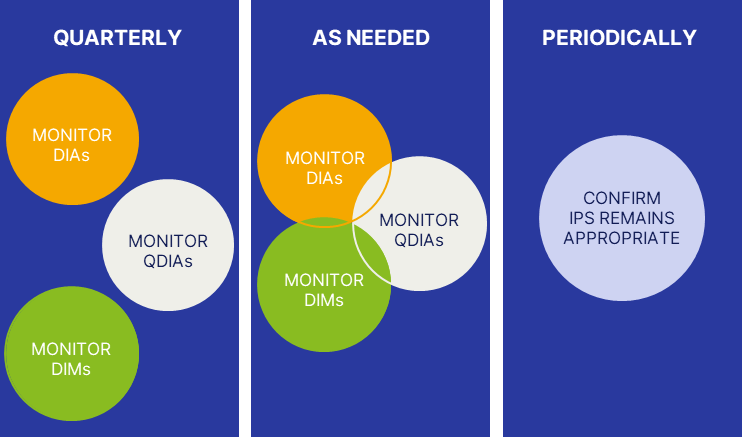

Once the appropriate number of types of DIAs are selected, then the fiduciaries (in consultation with the plan’s investment professional) should periodically monitor the funds to ensure they continue to be appropriate based upon the objectives set forth in the IPS. If they are not, the fiduciaries should replace the DIA with one that meets the IPS criteria.

A properly drafted IPS can be a valuable tool to help the plan’s fiduciaries manage their investment-related risk. It can reduce the time plan fiduciaries spend selecting, monitoring and replacing investments for the plan by streamlining decision-making and required documentation. At a minimum, your IPS should include the following:

- Identification of the plan’s fiduciaries responsible for investment-related decisions;

- Investment objectives of the plan and the role of service providers;

- Description of any investment philosophies or fee policies to be considered that may limit the universe of available investments;

- Process for selecting and replacing DIAs and, if applicable, model asset allocation portfolios (Models), qualified default investment alternatives (QDIAs) and/or designated investment managers (DIMs) available through the plan; and

- The frequency at which the DIAs, QDIAs, and DIMs will be monitored (e.g., quarterly, semi-annually, etc.).

There is no perfect formula or checklist for creating an IPS; the key is to have criteria for assessing investment options and follow that criteria. Generally, the plan committee in conjunction with the plan’s investment advisor or consultant will draft the IPS with assistance from legal counsel if necessary. Many retirement plan service providers will offer template IPS forms; however, to be effective, each IPS should be customized to the extent possible to match the needs of the plan participants and beneficiaries.

Generally speaking, plans with less investment savvy employees should have fewer DIAs and promote diversified, age- or risk-appropriate investing through Models and/or QDIAs. Plans with more sophisticated employees may find it prudent to offer more DIAs or even self-directed brokerage accounts from which the participants can create their own diversified portfolios.

The IPS should be a guide for decision-making, but not a mandate as to how and when funds should be added and replaced. It needs to appropriately reflect the plan’s investment philosophy while creating rules and benchmarks upon which to administer the evaluation process. Generally, this would include rules for investment manager selection and termination, basic fund evaluation criteria, and parameters with respect to when investment options should be put on the watch list.

In addition, you should review the policy periodically to ensure compliance with the document, as well as make adjustments according to the needs of the plan. Keeping an IPS up to date will help to demonstrate you are meeting your fiduciary duties.

SPECIAL CONSIDERATIONS FOR QDIAS

ERISA allows participants to be automatically invested in a QDIA when they are automatically enrolled in the plan and/or fail to direct the investment of their individual accounts. Plan fiduciaries are relieved from liability so long as they can demonstrate that the plan’s QDIA is prudently selected and monitored and certain procedures are followed.

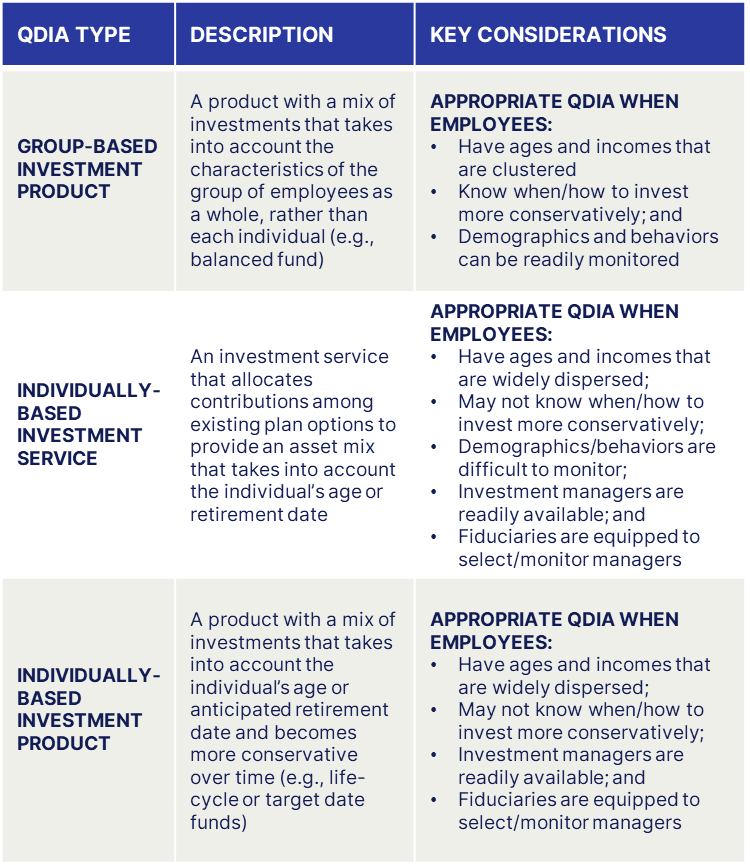

There are four types of QDIAs; however, the fourth “capital preservation” option is a short-term only option for the first 120 days of participation in the plan. The three standard QDIA types and key considerations are outlined below:

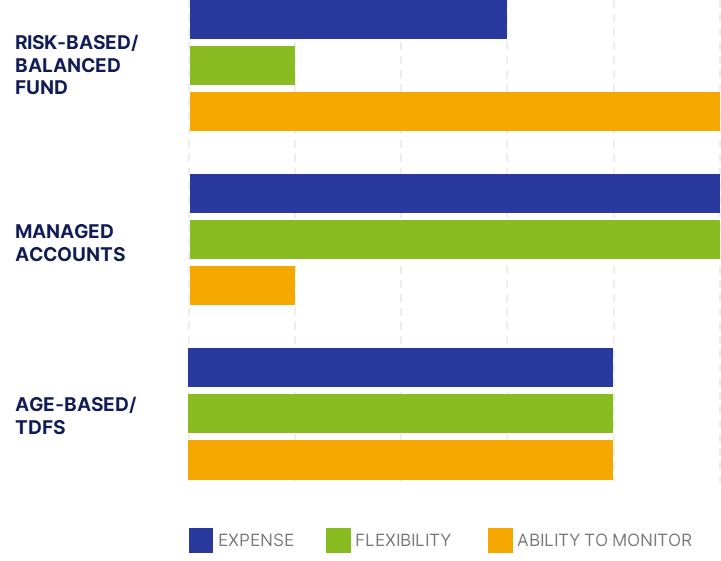

While there are benefits and challenges associated with implementing each of the QDIA types, the chart below outlines some additional considerations:

Given that the majority of defaulted participants tend to remain invested in the QDIA, you should work closely with your plan’s advisor or consultant to ensure that you have selected an appropriate QDIA and are providing the required notices and disclosures – particularly if you select a target-date fund – as the DOL has issued additional Tips for ERISA Plan Fiduciaries that should be considered.

Given that the majority of defaulted participants tend to remain invested in the QDIA, you should work closely with your plan’s advisor or consultant to ensure that you have selected an appropriate QDIA and are providing the required notices and disclosures – particularly if you select a target-date fund – as the DOL has issued additional Tips for ERISA Plan Fiduciaries that should be considered.

A properly implemented QDIA can not only significantly mitigate your fiduciary risk as a plan sponsor but can go a long way in helping participants save appropriately for retirement.

WORKING WITH 3(38) INVESTMENT MANAGERS

ERISA permits plan fiduciaries to delegate day-to-day responsibility for selecting all or a portion of the plan’s investments to an “investment manager.” If properly appointed and monitored, the fiduciaries will not be liable for managing those investments over which the investment manager exercises discretion.

If you determine that it is necessary to engage an investment manager, there are a number of considerations you will need to document to ensure you have effectively delegated your duties. The following questions are designed to help you select and monitor an investment manager:

- Is the investment manager a bank, registered investment advisor

- or insurance company?

- Does the investment manager acknowledge his/her fiduciary status in the contract with the plan, and are the other terms reasonable?

- Does the investment manager have the requisite background, experience and/or insurance to perform the services?

- Is the investment manager properly licensed and in good standing?

- How is the investment manager compensated, and does that present any conflicts of interests?

- Is the value provided reasonable in light of the compensation received by the investment manager?

- Are participants satisfied with the services provided?

It is also important to consider what functions the investment manager may not be willing or able to perform. Often times, the manager’s services may be provided remotely and/or limited to managing the plan’s DIAs, QDIAs and/or participants’ accounts.

In these cases, it may still be necessary to engage a local plan advisor or consultant to help with other aspects of the plan (i.e., providing advice or education to participants directly, helping the fiduciaries select and monitor the plan’s service providers, including the investment manager, etc.). The table below shows that the distinctions among the various types of investment professionals relate primarily to their investment-related functions.-1.png?width=750&height=247&name=3(38)-1.png)

FIDUCIARY CONSIDERATIONS FOR BROKERAGE WINDOWS

Some plans may offer the ability to invest outside the plan’s DIAs, QDIAs or DIMs through a self-directed brokerage account (SDBA). In many cases, these SDBAs allow participants to invest in stocks and bonds in addition to mutual funds and ETFs. While plan fiduciaries will typically not be liable for a participant’s investments made through an SDBA, the decision to offer SDBAs is a fiduciary act in and of itself. Consequently, you should carefully evaluate whether or not SDBAs are appropriate for your participants. Before coming to this decision, you may wish to consider the following:

- Is the participant population sophisticated enough to benefit from the ability to invest in the universe of securities available through the SDBA?

- Should a minimum balance in the participant’s core retirement plan account be achieved before the SDBA is made available?

- Will there be a limitation on what percentage of a participant’s total account balance can be diverted to an SDBA?

- What service providers, if any, will be available to assist participants in making prudent investment allocation decisions?

- Is the service provider offering the SDBA able to adequately meet the needs of the participants at a reasonable cost?

- How will investments made through the SDBA affect the allocation of administrative costs of the plan among all participants?

If you determine that an SDBA is a necessary plan feature, then you are required to include a description of the SDBA features, limitations, fees and expenses, at least annually, to participants as part of their 404(a)(5) participant-level fee disclosures. In addition, you want to consider having participants acknowledge the risks of investing outside the prudently selected and monitored DIAs, QDIAs and/or DIMs.

While fiduciaries cannot disclaim away their fiduciary duties, providing additional acknowledgments can serve as a reminder to the participant regarding the benefits available through the plan’s traditional investment options or serve to show they assumed the risks of investing through the SDBA.

- Acknowledgments to consider include, but are not limited to:

- risks associated with making investments through the SDBA;

- SDBA investments are not reviewed or approved by the plan sponsor; and the participant is solely responsible for all SDBA investment decisions.

Even with adequate disclosure, plan sponsors have a fiduciary obligation to review whether offering a brokerage window is in the best interest of the plan participants. Simply offering a brokerage window does not abrogate the plan sponsor’s fiduciary liability with respect to the core investment options available to plan participants; it also does not relieve them of their responsibilities to prudently monitor the associated fees and costs of administering the plan with a brokerage window option.

FIDUCIARY CONSIDERATIONS FOR SOCIALLY RESPONSIBLE INVESTMENTS

In recent years, socially responsible investing has become increasingly important to many plan sponsors. A term commonly used to describe this concept is ESG investing, which gains its name from "environmental, social, and governance" factors investors may consider when selecting an investment. In the context of employer-sponsored retirement plans, it is important that plan sponsors follow an objective process when evaluating ESG investments to be included in their plans.

The need to follow an objective process when selecting investments is not unique to ESG options. As noted earlier in this guide, fiduciaries are required to consider relevant information (or that which they should know to be relevant) about any investment options available to the plan. Additionally, fiduciaries to participant-directed plans are required to select an appropriate number and type of investments so that participants can create well-diversified portfolios to minimize the risk of large losses.

With those factors in mind, before deciding whether to include ESG investments in your employer-sponsored plan, you should consider the following:

- Are the ESG investments under consideration otherwise consistent with the Plan’s Investment Policy Statement?

- Is the performance of the ESG investment under consideration comparable to other non-ESG investments available for inclusion in the investment line-up?

- Is the risk profile of the ESG investment under consideration comparable to other non-ESG investments available for inclusion in the plan’s investment line-up?

- Does the plan contain an appropriate number of non-ESG investments that are consistent with the Plan’s Investment Policy Statement?

In addition to the above, it is important to note that not all ESG investments use the same screening criteria when determining social responsibility. Sponsors who wish to pursue adding ESG investments to their plans should conduct a thorough review to determine which criteria the investment manager is using for the fund to be considered socially responsible.

Plan fiduciaries must also be careful when considering social activism related to proxy voting or otherwise managing plan investments. Plan fiduciaries may not increase expenses, sacrifice investment returns, or reduce the security of plan benefits to promote collateral goals, including proxy voting.

Lastly, recent guidance from the DOL strongly advises against using an ESG investment as a QDIA. As noted earlier, plan sponsors receive protection under ERISA when selecting QDIAs so long as they demonstrate that the QDIA is prudently selected and monitored, and certain procedures are followed. Recent DOL guidance indicated that selecting an ESG investment as a QDIA would bring into question the fiduciary’s prudence and compliance with the duty to act solely in the interest of the plan’s participants and beneficiaries. For more information, please see the DOL’s Field Assistance Bulletin 2018-01.

POLICIES AND PROCEDURES: WITH INVESTMENTS

With respect to selection of investments for the plan, ERISA requires you to follow an objective process. In order to make well-informed decisions, you are required to consider relevant information (or that which you should know to be relevant).